The Shape of Commodity Cycles

Most investors tend to think about commodities as a single decision. Own them or don't. Set an allocation and leave it alone. Treat them as a hedge against inflation and rebalance occasionally. This framing is intuitive, but it may not fully reflect what matters in commodity markets.

Commodity prices move on multiple timescales, driven by very different forces. Long-duration cycles emerge from structural shifts in capital investment, technology, and productive capacity. These can play out over decades. Shorter cycles emerge from discrete shocks — wars, pandemics, supply disruptions, demand collapses. These typically play out over months to a few years. Both produce inflation pressure. Both can matter for portfolios. But they require different analytical tools and different positioning decisions.

Commodity cycles are not a single phenomenon. The discipline of distinguishing between them is a core part of how we think about real-asset exposure.

Structural Cycles

Long-duration commodity cycles exist because capital in real-asset industries is slow. A new mine takes roughly a decade to develop from discovery to production. Power generation and transmission infrastructure require years of permitting and construction before delivering a kilowatt-hour. The physical economy cannot respond quickly to changes in demand. When demand outruns existing capacity, prices must clear the imbalance for long enough to incentivize new supply — and incentivizing new supply takes time.

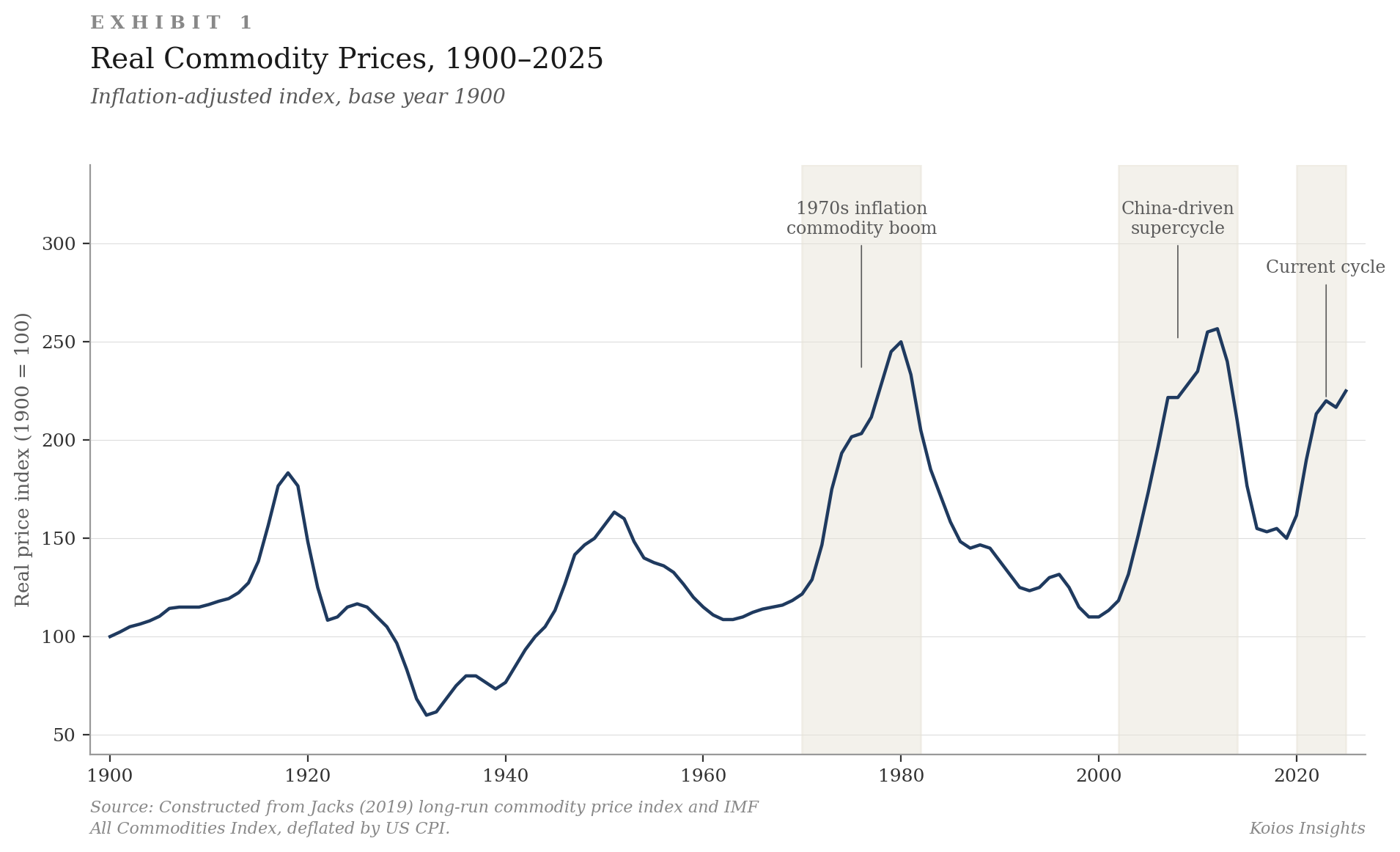

This dynamic produces cycles measured in decades rather than quarters. The post-war industrial reconstruction drove one. The 2000s emerging market industrialization, particularly the China buildout, drove the most recent and most-studied commodity supercycle. Both were grounded in structural demand shifts that took years to develop and years to resolve. Both reshaped global commodity markets in ways that were not fully apparent until well after they had begun. The long-duration pattern is visible in the historical record (Exhibit 1).

The current example worth observing is the AI infrastructure buildout. Whatever its eventual effects on the cost of cognitive labor, its near and medium-term effects on physical inputs run in the other direction. Data centers require electricity at a scale that strains existing grids. New generation capacity requires turbines, transformers, copper, steel, and uranium. Cooling systems require water and specialized materials. The physical capital intensity of this transition is substantial, and the lead times for the supply response are measured in years. This is the kind of structural force that drives long-duration commodity cycles. We mention it not to make a specific forecast, but to identify the kind of dynamic the framework is watching.

Shock-Driven Cycles

Shorter commodity cycles operate on different terms. They are triggered by discrete events — geopolitical disruption, conflict, natural disaster, pandemic — and produce sharp price moves that can persist for months or years before resolving. They can produce meaningful inflation regimes, particularly when they hit energy or food markets. But their causes are episodic, and their duration depends on whether the underlying disruption gets repaired, replaced, or absorbed.

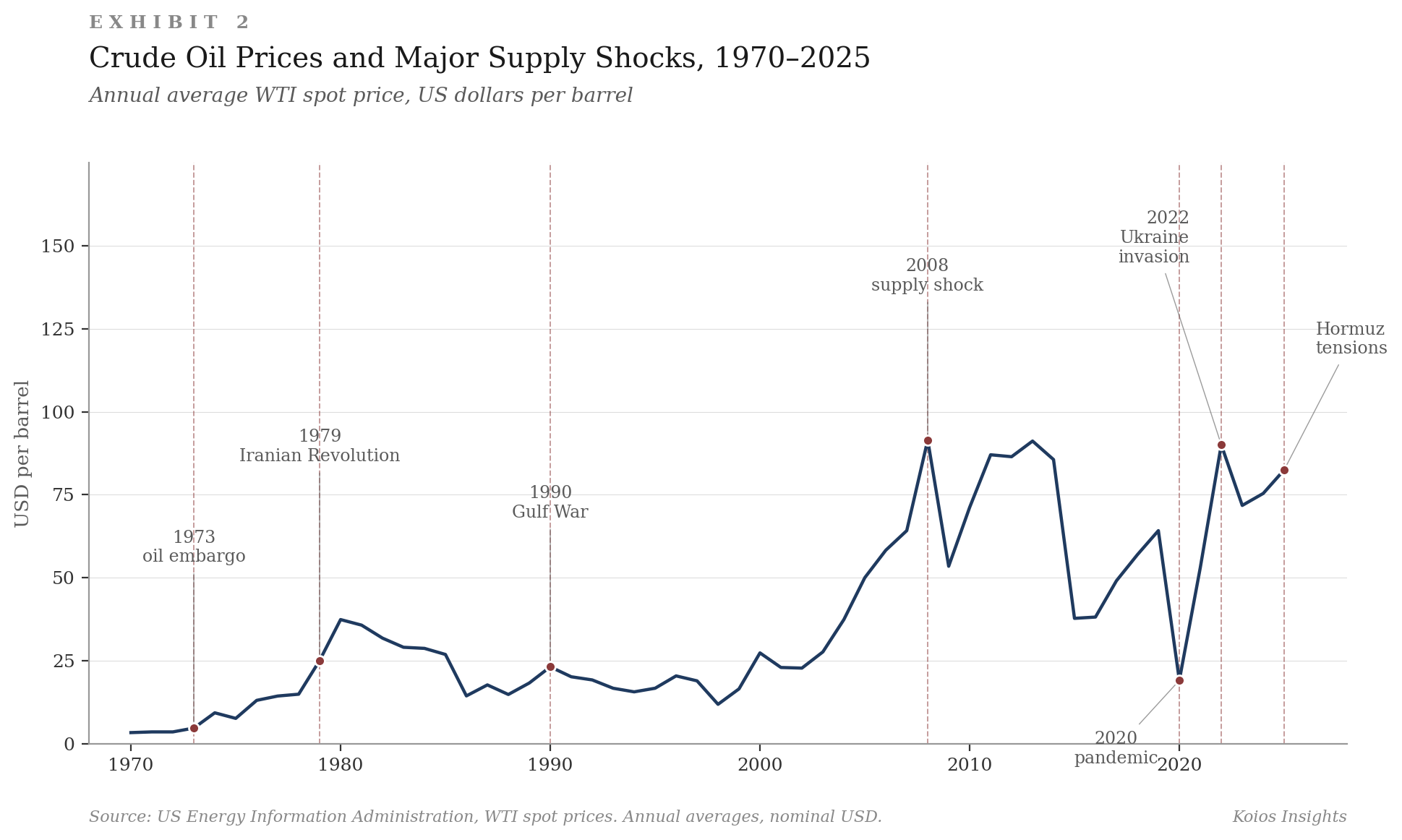

The 1970s oil shocks are the canonical example. The 1990 Gulf War. The 2020 pandemic supply chain disruption. The 2022 Russian invasion of Ukraine and the subsequent European energy crisis. Each produced significant price action and policy response. Each resolved on its own timeline. The current tension around the Strait of Hormuz fits this category — a present-tense example of the kind of supply-side fragility that may produce a meaningful price response when underlying conditions are already tight. Crude oil prices show the pattern clearly (Exhibit 2).

Shock cycles can be loud. Their longer-term portfolio implications depend heavily on whether they coincide with a structural cycle that amplifies them.

When Cycles Compound

The 1970s remain the most instructive period in modern commodity history. A structural commodity cycle was already underway by the late 1960s, driven by post-war demand growth and the gradual exhaustion of cheap reserves built up in earlier decades. The 1973 and 1979 oil shocks landed on top of that structural condition. The combination produced the most damaging inflation regime in modern U.S. history and the worst stretch for traditional balanced portfolios in the post-war period.

The lesson is not that shocks cause inflation. It is that shocks landing during structural cycles produce materially different outcomes than shocks landing during quiet periods. The same supply disruption — same magnitude, same duration — can produce a brief price spike that fades within months, or it can compound a structural condition into a multi-year regime. The difference depends on what was already in motion underneath. Today’s environment has both structural drivers and recurring shocks. The framework must distinguish between them while also recognizing when they are compounding.

What This Means For Investors

The conventional approach to commodity exposure is binary. Often client portfolios either have no commodity allocation or a fixed allocation set once and rarely revisited. Both approaches assume commodities behave the same way over time, which they do not. A structural cycle that runs for a decade looks nothing like a shock that resolves in eighteen months. Treating them identically may be an oversimpliciation, and over a long horizon it has real portfolio consequences.

Our view is that commodity exposure is not a single decision. It is a recurring set of decisions that depend on which kind of cycle is operating, where we are within it, and whether multiple cycles are compounding. The framework treats long-duration structural cycles and shorter shock-driven cycles as different problems with different solutions. We do not believe a single static allocation captures either, nor we do not believe commodities should be treated as a fixed slice of a portfolio independent of the underlying conditions. This is one of the places where disciplined cycle analysis shapes how exposure is constructed.

Closing

The point is not to predict the next cycle or call the next shock. It is to have a framework that recognizes the difference between them and adjusts portfolio exposure with that distinction in mind. That discipline is most of what separates more systematic commodity investing approaches from speculation.

How that framework translates into specific portfolio decisions depends on the individual client — their existing exposure, their objectives, their time horizon, their tax circumstances. The conceptual work is what we make public. The portfolio work happens one client at a time, in the context of each relationship.

It is how we approach the question. It is why we think clients with meaningful long-term capital should expect their real-asset exposure to be analyzed with the same nuance applied to any other significant allocation decision.

Disclosure

Koios Private Family Offices, LLC · This material is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.